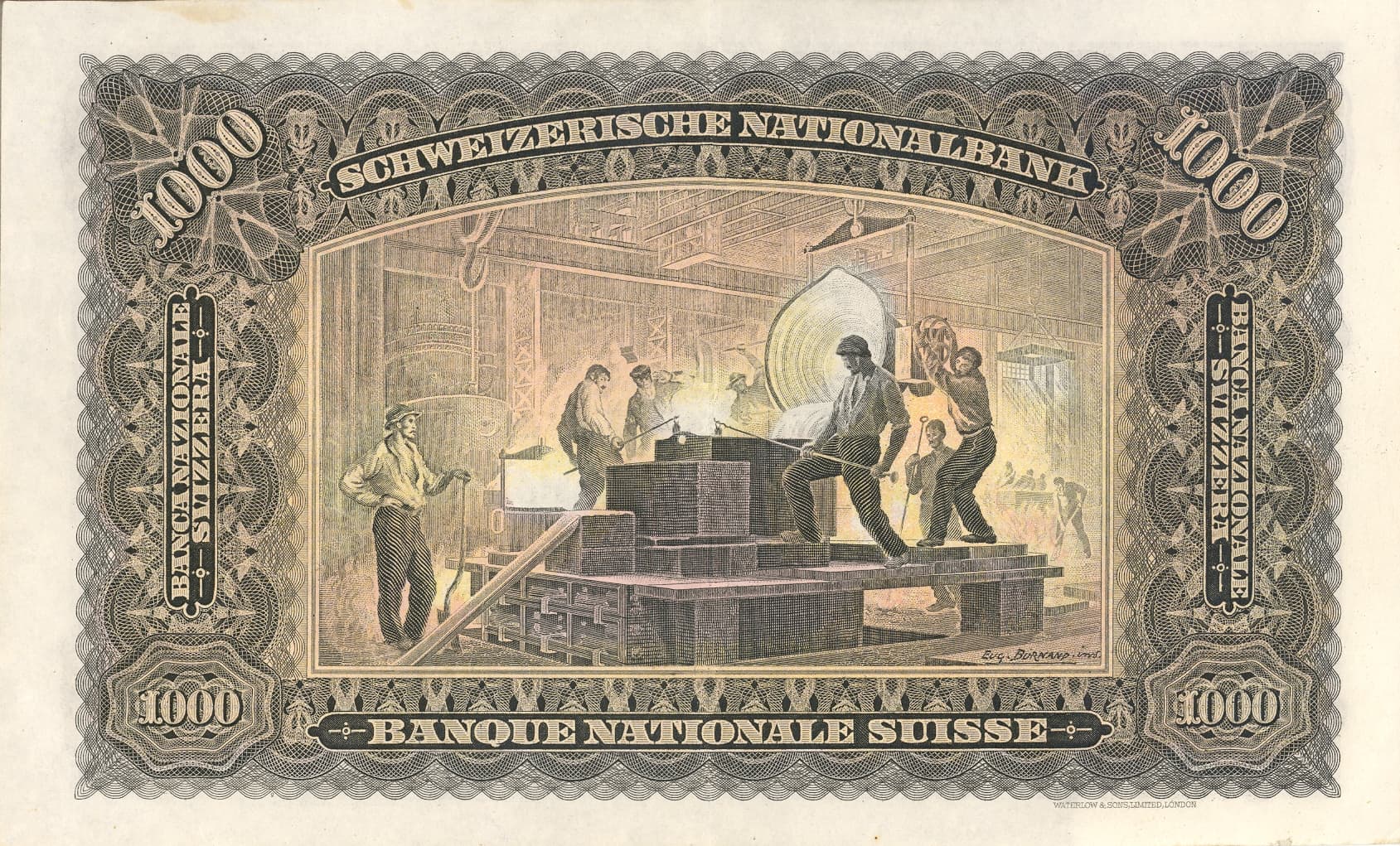

In 1911, when the Swiss National Bank issued the second series of its banknotes, it chose for the thousand-franc note — then one of the most valuable pieces of paper a person could carry — an engraving by the painter Eugène Burnand of men at work in a foundry. The image was not subtle. Money, the note insisted, is a condensed form of labour; value is something a country makes. For most of the century that followed, Switzerland made a different product, less photogenic than molten metal but more profitable: the safekeeping of other people's fortunes, performed with a discretion so reliable it functioned as a natural law.

A hundred and fifteen years later, almost to the season, the Boston Consulting Group informed the country that the law had been repealed. In its Global Wealth Report 2026, published at the end of May, BCG put Hong Kong's cross-border wealth — money managed in one place for people who live somewhere else — at 2.95 trillion dollars, against Switzerland's 2.94 trillion.1 The margin is a few billion dollars, a rounding error in the accounting of global wealth. But rankings are not arithmetic; they are stories, and this one ends a reign that lasted longer than most countries' constitutions. Hong Kong and Singapore are projected to grow at about nine per cent a year through 2030, Switzerland at roughly six.1 Deloitte's longer-running ranking tells the same story in slower motion: the Swiss share of internationally managed wealth has drifted from nearly twenty-four per cent before the pandemic to about twenty-one.2

The Swiss reaction was, in its way, perfectly Swiss. The country's bankers pointed out, correctly, that Hong Kong's ascent says more about where new wealth is being created — above all in China — than about anything Switzerland has done wrong. And the new champion's crown sits less securely than the headline suggests: within days of the BCG report, Bloomberg reported that Beijing had told the city's large online brokerages to wind down their mainland-client accounts within two years — a reminder that the wealth pulling Hong Kong upward answers, in the end, to politics.3 Switzerland's product has always been the opposite promise: that the money answers to law.

So this is not decline, exactly. Switzerland still anchors UBS, which ended last year managing more than seven trillion dollars of client money, and the country has assembled the most complete regulated infrastructure for digital assets of any major financial centre. But something more basic than a ranking has shifted. Swiss banking was built on weight — vaults, granite, the accumulated gravity of a century of kept secrets — and money has spent the past generation losing its weight. It moves as code, settles in seconds, owes nothing to geography. The centre of that lightened wealth is drifting east, the technology underneath the industry is being rewritten, and the generation about to inherit the money chooses a bank for reasons their parents would not recognise. The question Burnand's foundry puts to its successors is whether the country can manufacture a new kind of gravity.

The question is not whether Switzerland stays relevant. It is whether the first-mover stack ages into real infrastructure.

From first-mover advantage to industrial scale

Three technological shifts are remaking banking at once, and Switzerland's position on each is different.

The first is generative and agentic AI, where the era of pilots is over and the operating question is now live. The consultants' arithmetic is blunt: BCG estimates that a wealth manager rebuilt around AI can free a quarter to a third of its advisors' working hours and lift the revenue each advisor produces by fifteen to twenty per cent.4 For a financial centre whose chief handicap is how expensive it is to run, this is the first credible offer in twenty years to make a Swiss bank cheaper to operate without simply firing the people who are the product. Which makes AI, for Swiss banking, less a growth story than a survival tool. If it doesn't make the bank measurably cheaper to run within twenty-four months, it is theatre.

For Swiss banking, AI is less a growth story than a survival tool. If it doesn't make the bank cheaper to run within twenty-four months, it is theatre.

The second shift is the migration of stocks, bonds and funds onto blockchain rails — "tokenization," in the industry's word, which means recording who owns what on a shared digital ledger rather than in the back offices of a chain of intermediaries. Switzerland got there first, and what has happened to that lead since is the most instructive story in Swiss finance.

In 2021, the operator of the national stock exchange won the world's first full licences to run a venue — the SIX Digital Exchange, or SDX — where securities issued directly on a blockchain could be both traded and kept safe under one regulator, FINMA. It went on to handle more than two billion francs of these digital securities, including bonds for UBS and the World Bank.5 Beneath it, the Swiss National Bank's Project Helvetia has, since the end of 2023, settled live digital-bond trades in actual central-bank money issued in tokenized form — a "wholesale CBDC," used only between banks — under a mandate that now runs to at least mid-2027. No other jurisdiction has lined up issuance, listing, trading, custody, tokenized commercial-bank money and central-bank settlement inside one regulated perimeter.

No other jurisdiction has lined up issuance, listing, trading, custody, tokenized commercial-bank money and central-bank settlement inside one regulated perimeter.

And yet the pioneer itself no longer exists. Over the past year SDX has been quietly taken apart: its trading operations were folded into the main Swiss exchange last October, and in May FINMA approved merging what remained into SIX's central securities depository — the vault-keeping utility that underpins the ordinary Swiss market.5 Read generously, this is what industrialisation looks like: digital securities cease to be a showcase and become default plumbing, and indeed Citi has just begun using that former SDX infrastructure to offer tokenized shares of private companies to its wealth clients. Read ungenerously, it is a burial with full honours.

The home team's behaviour supports both readings. When UBS launched its tokenized money-market fund in late 2024, it did so on public Ethereum — the open, global blockchain — rather than on home infrastructure; and when, last November, the bank demonstrated what it called the world's first in-production, end-to-end tokenized fund workflow, that too ran on public rails. Sergio Ermotti, UBS's chief executive, told analysts in February that his bank is a deliberate "fast follower" on blockchain. Even the word "only" in Switzerland's only-licensed-venue boast has expired: in March 2025, FINMA licensed a second digital trading venue, run by the Swiss arm of Germany's Boerse Stuttgart.

UBS ran its world-first tokenized fund workflow on public Ethereum — not on home infrastructure. Sergio Ermotti calls his own bank a deliberate "fast follower" on blockchain.

The third shift is the least glamorous and the most decisive: the modernisation of the core systems banks actually run on. AI does not sit cleanly atop forty-year-old mainframes; tokenized assets do not connect to ledgers designed in the punch-card era. UBS's absorption of Credit Suisse is the largest live demonstration in Europe of why legacy technology is simultaneously the cost problem and the precondition for everything else: the bank completed the migration of roughly 1.2 million clients this March — some 950,000 of them booked in Switzerland — and has so far decommissioned more than 1,100 legacy applications. Whether the country's mid-size banks finish their own, less publicised versions of that programme is the single most under-discussed determinant of who is still standing in 2030.

Legacy IT is simultaneously the cost problem and the precondition for everything else.

Principled. Slow. Outpaced.

Switzerland regulates finance the way it builds tunnels: from first principles, without haste. FINMA applies existing law, supplemented by guidance, to whatever technology arrives. The approach produced genuine firsts — the 2018 token-classification framework, the 2021 DLT Act, the first licence for a new-generation digital trading venue in March 2025. The machinery is still turning: a consultation on two new licence categories — one for issuing stablecoins, one for crypto custody and trading — closed in February, with the bill expected to reach parliament later this year and the licences unlikely to bite before 2027. In April, a consortium including UBS, PostFinance, Sygnum, Raiffeisen and the cantonal banks of Zurich and Vaud began piloting a Swiss-franc stablecoin in a supervised sandbox.

The competitive problem is not the substance. It is the velocity, and the packaging. The European Union's MiCA regulation created a single crypto licence valid across thirty countries, in force since the end of 2024; its last transition period expires on the first of July — three weeks from now — after which Swiss firms serving European clients comply in full or retreat. Sygnum, the Swiss digital-asset bank, is building its European access through Liechtenstein. Singapore's regulator counted more than two thousand single-family offices by the end of 2024 and approves their tax incentives in about three months. The Dubai International Financial Centre — a financial free zone with its own English-common-law courts — applies zero per cent tax on qualifying income, and the top families in its ecosystem hold 1.2 trillion dollars. Hong Kong wrote a stablecoin law last year and granted its first two licences this April, one of them to HSBC. All three move faster than Bern.

The competitive problem is not the substance. It is the relative velocity and the packaging.

The clients no longer pick the bank their parents picked

The demand side, meanwhile, is being remade in three reinforcing directions.

The first is the largest transfer of wealth in recorded history. Cerulli Associates puts the cumulative American figure through 2048 at 124 trillion dollars — roughly 105 trillion flowing to heirs, 54 trillion passing first between spouses, and nearly 40 trillion of those spousal transfers going to widowed women before reaching the next generation.6 Heirs, it turns out, fire their parents' advisors with striking regularity at exactly the moment the money moves — which makes courting the next generation, onboarding them digitally, and helping families govern themselves existential work rather than a marketing line.

The second is the migration of private markets — stakes in companies, credit and property that don't trade on any exchange — from the preserve of pension funds and endowments into the ordinary portfolios of wealthy individuals. Preqin now expects these private assets to reach thirty-two trillion dollars by 2030, with private individuals supplying most of the new money.7 This plays directly to what Swiss banks have always sold — portfolios managed on the client's behalf, advice tailored by hand — and intersects naturally with tokenization, which promises to make such illiquid holdings tradable.

The third direction sits underneath the other two: geography. Wealth is increasingly created and held in Asia and the Gulf, which is why UBS leads wealth management in Singapore and Hong Kong from the ground rather than from Zurich alone.

An expensive home, a single champion

The structural weaknesses are well diagnosed. Swiss banks are expensive to run, and the easy money is gone: the Swiss National Bank cut its policy rate to zero a year ago, ending the brief windfall banks had enjoyed from interest, and has held it there since. When its rate-setters meet next Thursday, the expectation is another hold — and the live debate in the markets is whether the strength of the franc eventually forces the next move to be a small hike, not a cut. Either way, nobody in Swiss banking is planning around easy interest income again.

Consolidation is doing what consolidation does. KPMG projected the number of Swiss private banks would fall below eighty by the end of last year — there were about a hundred and sixty in 2010 — and the period's biggest deal, Safra Sarasin's purchase of Saxo Bank's Swiss business, made the threshold plausible; this year's edition of the survey is due within weeks.8 Two business models reliably make money: very large banks that do everything everywhere, and small ones that do one thing exceptionally. The middle is being squeezed out of existence.

Which leaves the champion. UBS earned 7.77 billion dollars last year, expects to substantially complete the Credit Suisse integration by December, and has already banked eleven and a half of the thirteen and a half billion dollars in savings it promised. Its scale is now singular: more than seven trillion in client assets, the number-one wealth manager in both Hong Kong and Singapore. But concentration is risk, and Switzerland and its champion are currently negotiating the price of each other's company. In April, the government sent parliament a bill requiring UBS to fully back its foreign subsidiaries with capital held at home — roughly twenty billion dollars of extra capital, on the bank's reckoning, phased in over years. This week, Reuters reported that lawmakers are weighing a softer compromise, nearer fifteen billion.9 Ermotti, asked at the Swiss Economic Forum this month, said: "We absolutely want to stay in Switzerland" — the sort of sentence that reassures chiefly because it needed saying.

Switzerland's global standing now rests heavily on a single institution.

What is owed to the next decade

Switzerland's position in 2026 is not the position it held in 2006, and the next decade will not be kinder than the last. The competitive baseline has shifted from leadership to contestation. The country retains assets no rival combines in quite the same way: a single bank of planetary scale, the most coherent regulated digital-asset stack anywhere, and the structural pull of neutrality and the rule of law — the old promise that the money answers to courts, not to politburos. What is required now is the unphotogenic work Burnand would have recognised: industrialising the tokenization stack rather than embalming it, deploying AI against the cost of running a bank, finishing the unglamorous replacement of the systems underneath, and rebuilding the advisory product for a generation that will not inherit its parents' loyalties. Money has gone light; the work now is to give it a reason to land here anyway. The next five to ten years will determine whether the platform becomes a working operating model — or a well-engineered museum.

This essay was written ahead of a companion panel on agentic AI, governance and AI-native models in banking and wealth management, to be hosted at wonderful.ai on Place de la Synagogue on 25 June 2026. The arguments will sharpen there.